For past issues of Syleconomics go to www.sylectus.com and see the “Hot News” section.

January 2013 vs. January 2012 had the same number of business days, so the 6% increase in trip count and 10% increase in revenue is a refreshing year over year increase. However, we continue to see rate erosion. The total revenue is up, but most of this increase is due to a higher fuel surcharge revenue.

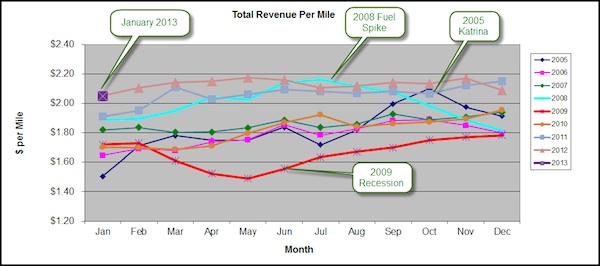

The January 2013 vs. December 2012 saw an increase in loads and business. January 2014 had about 20% more business days plus compared to December, so it would make sense that business would be higher than December. Again, what is more concerning is seeing a 2% drop in revenue per mile in just one month. January was a nice rebound after the fear of the “fiscal cliff” concerns. Those are now behind us.

Capacity is going back down. We noticed that capacity almost reached 2007 levels but has slowly retracted over the past few months .

Syleconomics commentary … Complaints about the rate per mile over the past 3 months.

It seems that whenever I publish our monthly Syleconomics report (sorry it was late this month … our annual user group planning consumed much of my time), I receive email responses from some recipients complaining about the rate-per-mile they are receiving from the network recipients.

Before I start, let me be clear that Sylectus and any affiliated company will not dictate or recommend rate/mile policies among Alliance participants. The trucking industry operates in a “free market” environment in North America so rate/mile negotiations are done strictly between the buyer and the seller.

So, let’s look at the rate/mile and understand how it is influenced.

First, there is seasonality in the trucking industry. By mid-December, most of the pre-Christmas shipping rush is complete and many people / organizations are gearing down for the holidays. The seasonal drop in shipments does not really pick up until around mid-February. Last year (in 2012) there were several anomalies that affected rates including a few severe snow storms and other one-time events that tended to keep volumes and rates up. By contrast, this year saw very moderate weather patterns that did not disrupt/strain supply chains. So seasonality, predictability and stability within transportation put downward pressure on rates.

Second, there is supply/demand at play. We are seeing more entrants into the trucking industry (both at the small company and individual driver level). Our capacity index (see the green line in the above chart) is showing that truck/driver availability continues to inch upwards. Couple this increased availability with lower seasonal demand (shipment count) and rates will fall (or remain stable). The table above shows that rate/mile has increased year-over-year, but rate/mile has remained relatively flat in 2012 compared to 2011, even though trips (demand) increased.

Third, the complaints I hear about rate/mile reductions are often from the smaller carriers that do not have a large customer base and rely on load boards for most of their business. Companies with larger, diversified customers as well as brokering authorities are able to maintain their rates (during the slower months) due to contracts and market strengths.

Fourth, I had some interesting discussions with customers at our annual convention in Scottsdale a few weeks ago regarding companies who have been dropping rates to gain market share. Although this is a proven method to gain market share, it does not guarantee the ability to maintain market share. Shippers are notorious for changing carriers for a penny a mile savings. At our annual convention in Scottsdale our morning keynote speaker, Mr. Michael Vickers, provided some valuable insights into how to become the preferred supplier without sacrificing rate. Wise companies attending the meeting will use these strategies to retain and gain market share without compromising rates.

Fifth, the rate/mile data we publish is a mixture of data that combines all sorts of business segments. It includes different vehicle sizes (cargo vans up to tractor trailer), different vehicle types (dry van, flat bed, reefer), different geographies (U.S., Canada, Mexico) and different industries served (automotive, pharmaceutical, high-tech, etc.). So, if you are a company with a fleet of cargo vans and sprinters serving the automotive market in the Midwest, your rate/mile experience could be completely different (better or worse) than a dry-van truckload operation moving high-valued computer electronics on the east coast. Whenever people question me about the rate/mile data we publish, I always tell them to look at the trends, not the actual rate/mile. I ask them to compare their rate trend to the rate trend in our data. Also, to consider the type of industry they serve, the vehicle classes they run, and the geographical area they operate in. We do not provide data that granular in our charts, so you need to understand how you operate within your market segment.

In all the above analysis, the main rate determinant right now is seasonality. The good news is that the seasonality can also be beneficial. We are entering the second quarter of the year when manufacturing typically picks up, the Northern hemisphere warms up and people emerge from their winter hibernation and start buying again, and freight volumes tick higher. I suspect that when the March Syleconomics is published, rates will have ticked higher as well.

As I mentioned when I started this section, Sylectus cannot and will not recommend or dictate rate/mile values. We can help you by reporting trends and historical information. The wise companies use this information to assist in their rate setting policies.

What will the smart transportation companies do?

- Understand how seasonality will affect demand for your services and how it will affect your “spot rate” decisions.

- Review your pricing policies and strategies to ensure your rates remain price-competitive, yet have sufficient margin to maintain your business needs and make a profit.

- Look to the Sylectus Alliance to forge strong partnerships with other Alliance carriers. This will provide you with the flexible capacity to still say “yes” to your customer, even though you may not have your own truck available.

- Network with your Sylectus Alliance partners. A great way to meet over 100 of these intelligent, forward thinking, progressive, growing companies is to attend our user group meetings. Watch for our announcement about our upcoming networking events.

- Build strong relationships and smart contracts with your key customers.

- Invest in technologies that will reduce your costs and improve your customer service and/or driver retention. If you are not using the Sylectus Alliance Pro software, ask us for a demo. Better yet, ask our Alliance Pro customers how the technology works.

What is the impact of these market forces on Sylectus?

2013 is slightly ahead of 2012 already as many companies have reached out to us asking to move up to Alliance Pro. What’s holding you back?

Supply/Demand analysis

2011 was the best year ever for many Sylectus customers. 2012 started out ahead of 2011, but the last 6 months of 2011 tracked with 2012. We see a particularly strong increase in our long-term customer base (customers with us for at least 5 years). The long-term customers have such a strong, well-established, trusted network within the Sylectus Alliance, that they have been able to leverage the Alliance capacity into higher business volumes.

Our SUPPLY-DEMAND index is comprised of a subset of our customers that have been on our system for a minimum of 6 years.

Capacity is going back down. We noticed that capacity almost reached 2007 levels but has slowly retracted over the past few months.

In contrast, the Dow Jones is now back at 2007 highs.

What is driving this success of our customers is not a strong, rebounding economy, but rather a continued and prolonged shortage of capacity. We are beginning to see an equilibrium reached between supply and demand which is stabilizing rates.

Total revenue per mile is a combination of

- Line-haul revenue per mile,

- accessorial revenue per mile and

- Fuel revenue per mile.

So what does this tell us?

- Supply of trucks (capacity) continues to lag below demand and has slowly recovered. It is now at the pre-recession levels. This is reflected in a stabilized line-haul rate per mile.

- The Demand (loads) is tracking better than 2007. 2010 and 2011 were great rides. 2012 started out ahead of the same period last year, but the last 6 months of 2012 tracked 2011.

- The survivors of the recession are reaping the benefits of the business volume uptick.

You still need to remind your operations staff to become “creative” when presented with load opportunities. Get them to use the software solution to:

- Turn every load opportunity into an order

- Turn every order into repeat business

- Keep your drivers happy.

Working together as a team (Alliance) can help weather any seasonal economic slowness and take advantage of the seasonal busier times (never saying “no” to a customer).

It just keeps getting better … and the best is yet to come!

About Sylectus

Sylectus is trucking’s most powerful network. Born in the new, cloud-based economy, it’s built on one simple idea … leverage the resources of your competitors to achieve extraordinary results for your customers and for your company. Sylectus is more than Transportation Management Software. It’s a web-based, protected, wealth creation network for managing in the New Trucking Economy. Designed exclusively forprogressive trucking companies, Sylectus enables them to bypass the investment and time continuum to grow fast NOW.